Analyse Economique

In Senegal, abandoning the CFA Franc is An economic and social demand to regain economic sovereignty, say Souleymane Gueye, professor of Economics, San Francisco College and Abdoulaye Cisse, Ph.D. Candidate, Department of Economics, University of California, Berkeley

Abstract

The recent economic events resulting from major external shocks such as COVID-19 and the Russian-Ukraine war and their impact on the Communauté Financière Africaine (CFA) franc zone have reignited the debate about the usage of the CFA franc in the West African Economic and Monetary Union (WAEMU). This article investigates how the economic performances of the WAEMU in general and Senegal, in particular, relate to the arrangements between the CFA Franc currency union and the Euro and between WAEMU and France. In particular, the paper analyzes the advantages and the disadvantages that stem from the different components of these arrangements and highlights the lack of economic competitiveness of the CFA franc countries caused by the structural overvaluation of the CFA franc, the lack of monetary and fiscal sovereignty, and the no optimality of the CFA franc zone as destabilizing elements of the CFA franc for WAEMU. The paper then proposes a mild reform in the short term and a complete abandonment of the CFA franc for a national currency anchored to a basket of currencies in the long term, in the hope of achieving inclusive growth and poverty alleviation in WAEMU.

Keywords: CFA franc, competitiveness, foreign reserves, development indicators, economic indicators, economic growth, poverty, debt, monetary policy, fiscal policy, exchange rate system, credit allocation

Introduction

While the debate over the usage of the CFA franc has been ongoing amongst economists since the early 60s, the issue has never been a major preoccupation of most Senegalese citizens for a long time. But in the last decade, a growing interest in using the CFA has been at the forefront of public/private media and social media[1]. This growing interest of the population in the economic issues surrounding the CFA franc should be welcomed and applauded by policymakers and politicians as it is time to examine objectively the benefits and the costs of the CFA franc’s peg to the euro and ponder about the economic performance of these countries and the role the currency is playing in fostering/hindering the capacity of these countries to alleviate poverty.

After more than sixty years of independence, it is not obvious that the currency is favorable to the economies of WAEMU in general and Senegal in particular.

Some economists say that the CFA franc affects the member countries in two key areas:

- Loss of sovereignty by tying the WAEMU’s economies to the French market and constraining the scope for an independent monetary policy; hence weakening the states with negative impacts on poverty alleviation

- The overvaluation of the currency impairs the competitiveness of exports.

Other economists argue that it has brought price and monetary stability, fiscal discipline, credibility, and stability to international competitiveness. Furthermore, they argue that a supranational central bank has insulated the CFA zone members’ economies from national treasuries. In contrast, the peg to the euro insulated a higher proportion of WAEMU’s trade from exchange rate fluctuations and encouraged regional convergence and integration.

These views have been reexamined and debated since the Macron/ Ouattara announcement to replace the CFA with the Echo (1). More voices are calling to sever the financial ties with France and completely abandon the CFA. The arguments for its abandonment range from “this currency is a relic of the colonial era,” “an instrument of the colonial era,” “an instrument of repression,” and “mean of exploiting the colonies.” Why is the CFA Franc, the currency many African countries use, so controversial?

This article aims to clarify this debate and supply economic arguments to justify severing the economic and financial arrangements at the core of the CFA franc zone.

What are the economic effects of the CFA franc’s peg to the euro? Should Senegal abandon the CFA franc as its national currency and issue its currency like many independent states or stay in the zone?

To answer these questions, we will present some institutional background on the CFA franc zone and briefly describe the economic structure of Senegal to provide the basis for an objective assessment of the effects (economic, monetary, and financial implications) of this exchange rate peg that convincingly should incentivize the future Senegalese authorities to exit the CFA zone and start the process of setting up the policy and institutional arrangements necessary for the introduction of a new currency.

I/ Structure / Architecture of the CFA Franc Zone

The monetary cooperation in the CFA franc zone is based on four key principles.

- A fixed exchange rate parity between the CFA franc and the euro remained constant from 1949 until 1994 when it was devalued by 50% to 1 French Franc = 100 CFA Franc which corresponds to 1 EUR = 655.957 CFA Franc since the euro replaced the French franc at the beginning of 1999, to help resolve a crisis that was associated with the overvaluation of the CFA franc and the failure of the structural adjustment policies imposed by the World Bank and the International Monetary Fund (IMF)(2).

- An unlimited and unconditional guarantee by the French Treasury for the convertibility of the CFA franc into euro at the fixed exchange rate at the Paris Stock Exchange. It is important to note that the warranty has not been used since the early 1990s, in contrast to the heavy mobilization seen before the 1980s.

- The centralization of the members’ net foreign reserves at the two central banks and until 2020, the obligation to deposit half of these reserves in an operating account at the French Treasury. Since April 2021, the operating account has been closed and the funds have been transferred to other WAEMU (West African Economic and Monetary Union) accounts, following the Macron Ouattara reform of 2019(3).

- Free capital movements within the CFA franc zone and with France although the central bank can impose exchange controls for transactions with non-member countries of the zone.

The closed operating account functioned like a current account with overdraft facilities and worked like a currency board arrangement, thus providing little scope for an active monetary policy. Consequently, an important indicator, the Reserve cover ratio (foreign exchange reserves/short-term liabilities of the central bank) was used to guide a passive monetary policy. The rule was such that when the reserve cover ratio dropped below 20% for three consecutive months, actions such as an increase in official interest rates and a decrease in refinancing ceilings must be taken to protect parity. In practice, the Reserve cover ratio never reached alarming levels as the WAEMU zone always kept the health levels of reserves. A similar indicator of coverage is the currency issue coverage ratio, which is the ratio of the foreign exchange reserves to the value of the physical currency in circulation (i.e., physical banknotes and coins).

Figure 1 shows that the requirement to maintain 50% of total foreign exchange reserves (represented by the blue horizontal line) has been respected by the WAEMU countries since 2007. While the share of total reserves kept at the French treasury has sometimes been close to the threshold, it has consistently been higher than that, which means that France has never had to trigger the guarantee that is theoretically in the arrangements. Figure 1 also shows that the coverage ratios have been at healthy levels and that WAEMU countries typically keep sufficient levels of foreign exchange reserves to cover most of the banknotes in circulation. This observation also points to the derisked environment in which the WAEMU countries operate.

Figure 1: Key Indicators Related to Foreign Exchange Reserves

Notes: This figure shows key indicators related to the reserves held in the operating account. The y-axis on the left (in blue) shows the share of total foreign reserves held in the operating account of the French Treasury. The y-axis on the right shows the currency issue coverage ratio, which is the ratio of the foreign exchange reserves over the value of physical banknotes and coins). The blue horizontal line corresponds to the minimum requirement of total reserves that need to be kept in the operating account. The red horizontal line corresponds to the minimum level of foreign reserves needed to cover the physical currency in circulation. All the raw data are from the annual reports of the WAEMU. All calculations are done by the author.

Before the closure of the operating account, the WAEMU countries were receiving an interest of 0.75% on their reserves deposited at the operations account (rates based on ECB interest rates.) In case these reserves turned into debt, interest was to be paid to the French Treasury. The French Treasury also guaranteed these reserves’ value against a depreciation of the euro vis a vis the Special Drawing Rights (SDR)[2].

However, several safeguards triggering action by the central bank are applied to ensure the exceptional character of foreign exchange interventions and to avoid a permanent reduction or deficit of the operating account. In case the account of a country goes into deficit for a month, a reduction of 20% of the refinancing ceiling is triggered for the culpable countries. When the surplus is less than 15% of the money supply for a country, a decrease of 10% of the refinancing ceiling is applied (4).

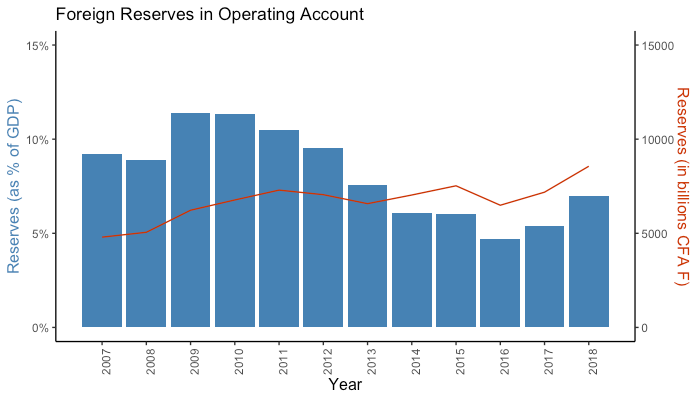

Figure 2 shows the level of foreign reserves held by WAEMU countries in the operating account at the French Treasury over time. Strikingly, we see that these reserves constituted a significant share of nominal GDP for these countries. They fluctuated 10% of nominal GDP between 2007 and 2018. Considering how funding and liquidity constraints WAEMU countries are, this stylized trend alone gives a sense of the drawbacks of the CFA franc.

Figure 2: Foreign Reserves Held by WAEMU in the Operating Account at the French Treasury

Notes: This figure shows the relative and absolute values of the foreign exchange reserves. The y-axis on the left (in blue) shows the level of foreign reserves that were held in the operating account as a share of the nominal GDP of the WAEMU countries. The y-axis on the right (in red) shows the nominal values of foreign reserves held in the operating account. The figure only includes foreign exchange reserves held in the operating account. The rest of the foreign exchange reserves not held in the operating account were excluded from the calculations. All the raw data are from the annual report of the WAEMU. All calculations are done by the author.

Given the safeguards described above, the time series of data in Figures 1 and 2, and the comparatively small size of the CFA franc zone economies, which currently represent about 5% of France’s GDP (Gross Domestic Product), the risks to France’s public finance remain limited in scope (limitation of potential liability of the French Treasury and at the same time supply a rule-based of credibility and to the fixed parity). It is quite unlikely for the account to go into deficit since it is based on the principle of pooling the reserves of the member states.

This safeguard mechanism was designed to control the “excesses” to which states are accustomed, taking away their ability to distribute internal capital resources through self-defined development strategies by allowing the central bank to impose a cap of 20% of national fiscal revenues on resource allocation to national treasuries of WAEMU countries.

For example, when the balance of the operation account is in deficit for three consecutive months, or when the ratio between net external assets and sight liabilities of a central bank is equal to or less than 20% for three consecutive months, refinancing amounts are reduced automatically by 20% and immediate corrective actions are taken by the board of directors, which is now fully composed of African officials and no longer has a French representative since the Macron Ouattara reform.

Therefore, it is the level of external reserves, and not credit needs, that decide credit allocation when it should have been the opposite. Credit allocation is decided by the French government’s monetary and fiscal authorities which will tend to perform it according to France’s view over the zone economies, not based on any development strategies developed by the WAEMU countries (5).

It should be noted that despite the closure of the operating account and removal of French representatives from the board of directors, the inherent structure of the CFA Franc is still such that it presents disadvantages and drawbacks to the WAEMU zone. Indeed, the terms of the guarantee of the CFA Franc and the Euro are still opaque and not fully transparent based on the latest public documents available. While the latest annual reports of the Central Bank of West African States (BCEAO) state that the operating account has now been closed, little to no details are given about the effective changes in the guaranteed mechanisms between the Euro and the CFA franc that resulted in this closure.

In what follows, we argue that France has clear benefits and few disadvantages with the current CFA franc arrangement.

II/ Disadvantages / Drawbacks for The CFA Franc Zone: What is wrong?

There are clear disadvantages and few benefits for the Franc Zone countries. The peg to the euro, before 1999 to the French franc constraints the scope for an active independent monetary policy of the WAEMU.

Overall, the arrangement has resulted in lower inflation (on average 8%) than in other countries in Sub-Saharan Africa, which have an average of 15%. But it has also significantly limited the macroeconomic policy options (fiscal and monetary policies as well as an exchange rate policy) available to the CFA Zone members (6). Indeed, the current exchange rate regime presents several macroeconomic problems that impede these countries’ ability to navigate external shocks such as the COVID-19 pandemic and Ukraine.

First, this principle compounded by a set of legal and institutional arrangements (Board composition and operations), as well as policy and operational features (design of supervisory arrangements within the two sub-zones[3]), are wrapped in a web of unwritten rules and practices with widespread consequences on the economic, monetary, financial, fiscal, and central bank policies of the entire CFA franc zone. Although there is no direct causation between these arrangements/ policies and development outcomes, the structural indicators of the countries in the CFA franc zone, such as the Human Development Index (HDI) and the Corruption Perception Index, are among the lowest in the world, and this suggests some correlation between the CFA franc arrangements and CFA franc countries’ development outcomes (7). For example, the HDI for Senegal in 2023 is 0.512, which decreased by 0.39% compared to the previous year with a rank of 170 while the average for the WAEMU is 0.544. These HDI values are below the HDI values of similar developing countries and none of the zone members is classified in the high HDI or Medium HDI categories in Africa. The extreme poverty rate is 27.5% (rank 32) and the GDP per capita is $1606 (rank 143).

As Table 1 below illustrates, the WAEMU region ranks the lowest in key development indicators including life expectancy, earnings, and schooling. While these figures do not imply any causational link between the currency the regions use and their economic indicators, the picture is still the picture: the WAEMU countries are some of the least developed countries by conventional standards.

Table 1: Development Indicators for Different Regions in the World

Table 1: Development Indicators for Different Regions in the World

| HDI | Life Expectancy | Years of Schools | GNI Per Capita | |

| Arab States | 0.708 | 70.9 | 8.0 | 13,501 |

| East Asia and the Pacific | 0.749 | 75.6 | 7.8 | 15,580 |

| Europe and Central Asia | 0.796 | 72.9 | 10.6 | 19,352 |

| Latin America and the Caribbean | 0.754 | 72.1 | 9.0 | 14,521 |

| South Asia | 0.632 | 67.9 | 6.7 | 6,481 |

| Sub-Saharan Africa | 0.547 | 60.1 | 6.0 | 3,699 |

| WAEMU | 0.486 | 60.8 | 3.4 | 2,692 |

Notes: This table shows some key economic indicators for different regions of the world. Each value shown is the mean of the variable in the first row for the region in the first column. The Human Development Index (HDI) is a composite index measuring average achievement in three basic dimensions of human development—a long and healthy life, knowledge, and a decent standard of living. (“Countries of the Third World – Nations Online Project”) Life expectancy at birth is the number of years a newborn infant could expect to live if prevailing patterns of age-specific mortality rates at the time of birth stay the same throughout the infant’s life. Mean years of schooling gives the average number of years of education received by people ages 25 and older, converted from education attainment levels using official durations of each level. (“Education Index | SpringerLink”) Gross national income (GNI) per capita is the aggregate income of an economy generated by its production and its ownership of factors of production, less the incomes paid for the use of factors of production owned by the rest of the world, converted to international dollars using PPP rates, divided by midyear population. All data are for the year 2021. All the raw data are from the UNDP website.

The persistence of monetary and financial relationships has favored neither structural transformation of the economies nor regional integration and has done even less for the economic development of the CFA countries. For example, 9 out of 14 countries in the WAEMU and the CAEMC zones are among the Least Developed Countries. With regards to health and education, CFA franc-using countries occupy the lowest ranks worldwide, as shown in Table 2.

Looking from a long-term perspective, average real incomes have stagnated or declined in five of the biggest CFA francs-using economies: Cote d’Ivoire, Cameroun, Gabon, Senegal (4.1% in 2022), and Congo Republic. Extreme poverty has risen by 3% since COVID-19. Countries in the CFA franc zone are the most impoverished in Sub-Saharan Africa despite stable prices (due to their lower inflation rate compared to the other countries in Sub-Saharan Africa). The average poverty rate for CFA countries stands at 40%. The opportunity cost of lower inflation has thus been slower GDP per capita and diminished poverty alleviation. All CFA Franc countries – including Senegal – are burdened by excessive debts and are in the category of Highly Poor Indebted Countries (HIPC)

MAJOR MACROECONOMIC INDICATORS

| 2020 | 2021 | 2022 | 2023 | |

| GDP growth (%) | 1.3 | 5.1 | 4.15 | 4.1 |

| Inflation (yearly average, %) | 2.5 | 2.1 | 9.7 | 6.5 |

| Budget balance (% GDP) | -6.4 | -6.3 | -6.2 | -4.9 |

| Current account balance (% GDP) | -10.9 | -13.3 | -13.2 | -14.5 |

| Public debt (% GDP) | 69.2 | 73.2 | 75.1 | 72.4 |

Source: World Bank Development Indicators and IMF: Debt, trade deficit, and other economic indicators

These observations are not surprising since these countries have an average credit-to-GDP ratio of 25% compared to an average of 60% for the rest of the countries in Sub-Saharan Africa and 148.5% for France. Furthermore, the amount of credit distributed to the CFA countries’ economies stays exceptionally low with prohibitive interest rates. Most of the loans are oriented towards the export sector and service sector to the detriment of investment in the primary and secondary sectors which employ more than three-quarters of people in the labor force. These countries face credit constraints, and financial repression, and cannot use interest rates to stimulate small and medium enterprises’ development because monetary policy is seriously constrained.

Second, the institution of the CFA is at the heart of the “colonial pact” set up by France in the 1960s when all these African countries were gaining their independence. Many critics of the CFA zone consider it a relic of Africa’s colonial past and a barrier to West African country’s economic progress.

Accordingly, the objective from its origin is to maintain peripheral economies that are ‘complementary’ to the French economy; otherwise, economies that serve as cheap sources of raw material supplies (consider how Senegal, Niger, Ivory Coast, and other countries in the WAEMU region are giving French companies licenses to exploit their natural resources).

Third, the peg to the euro decreases transaction costs and insulates French companies (and all foreign companies operating in euros for that matter) from exchange rate risk. Concurrently, it hampers the level of competitiveness of the domestic private sector in the zone by effectively acting as a subsidy to imports. As a result, most of the countries in the CFA zone run substantial trade deficits. For example, the trade deficit of Senegal stands at 10% of its GDP. Therefore, this structural overvaluation of the CFA franc – in 2020 the CFA franc in the WAEMU was 20% overvalued –, tends to favor imports, including luxury goods, to the detriment of exports. This is one of the reasons the political elite do not want to take the necessary steps to change the framework of the CFA franc zone.

Besides effectively contributing to subsidizing imports, the fixed parity also acts as a trade preference granted to the eurozone, since countries in the Franc zone cannot depreciate the exchange rate to affect the level of competitiveness of their exports or to absorb external shocks such as the Covid 19 or Ukraine war. Therefore, when confronted with trade shocks or crises, the only way to defend the anchor to the euro is a reduction in public expenditure (fiscal policy) and credits to the economy (monetary policy), as well as a recourse to external financing flows (more debt accumulation). In Senegal, public debt has been increasing at an exponential rate reaching 77% of GDP because of excessive borrowing by the government and state-owned enterprises to finance the budget and to invest in the oil and gas sector. The public debt service represents more than 50 % of fiscal revenue (1772 billion CFA francs, with interest payments and depreciation amounting to 502 billion and debt amortization to 1070 billion). The debt sustainability indicators are very close to their threshold (IMF Report, 2023).

The ratio of external debt service/export revenues is 19.1% for a threshold of 21% and the external debt service/ public sector revenue is 18.8% for a threshold set at 23%. This is very worrisome as it points to a severe constraint in the capacity to borrow money when faced with external shocks. The risk position of Senegal has deteriorated (from low to moderate-risk debt that can easily evolve to high-risk debt).

Fourth, the freedom of financial transfer eases the free investment and disinvestment of capital as well as the repatriation of profits, dividends, etc. This freedom is often associated with a massive capital flight -significant financial bleeding in resource-rich CFA countries such as the Republic of Côte d’Ivoire and Senegal (9),

Fifth, besides the handicaps of an overvalued exchange rate and capital outflows due to the outward transfer of local economic surpluses, the behavior of the banking sector keeps its colonial aspects. Most of the financial institutions are subsidiaries of French financial institutions despite the timid implementation of other foreign entities (Middle Eastern and North African countries)

Bank loans are primarily targeted at large companies and governments to the detriment of SMEs in general. This trend continues to hold despite the loss of market share of many French financial institutions in the CFA countries and the dominance of foreign banks. In Senegal, foreign banks control more than 90 percent of banking assets (10).

This situation explains the low level and inadequacy of the credits to the private and public sectors that hinder domestic production in the primary sector and manufacturing sectors. The overvaluation of the CFA franc worsens this decline in domestic production.

Sixth, the current system worsens inequality between urban elites and the rural poor by constraining incentives for commercial agriculture and subsistence agriculture. Furthermore, it has failed to accelerate growth for the poorest members.

Finally, although this monetary bond did not prevent the commercial and financial decline of France in its sphere of influence, it has nonetheless contributed to the institution of centralized political regimes that are more responsive to the priorities of the French government, French companies, and foreign investors than to the interests of their citizens. For example, in oil-exporting CFA countries such as Chad, Gabon, the Republic of Congo, and Equatorial Guinea, the ‘president for life’ model or president looking to extend their term by violating the constitution of their countries still is the norm, despite the frequent organization of formal elections with a foregone conclusion. Unfortunately, Senegal is heading that way with the current president’s determination to select his successor by preventing the main opposition leader from taking part in the upcoming election after awarding all the main public projects and exploitation of the key natural resources to French companies and other foreign entities (Turks, Chinese, Indian, and Middle Eastern countries as well as North African firms).

In other words, the CFA franc existence favors a particular type of political leadership. « Those who can aspire to lead CFA countries are those who will not question its limitations while those who question the underpinnings of the CFA framework will be jailed, exiled, or killed” (Sylvanus Olympio first president of Togo, Thomas Sankara of Burkina Faso). Leaders in the Republic of Côte d’Ivoire, Senegal, Benin, and Togo have enjoyed the active solidarity and support of the French government and the French private sector over the last six decades.

In the face of growing protests of this neo-colonial relic led by pan-Africanists, social movements, patriots, nationalist politicians, and academicians, France, in alliance with Côte d’Ivoire, decided in December 2019 to soften its stance on the West African CFA franc. This proposed reform is meaningless as it is extremely limited in scope. Its main objective is to prevent criticism by renaming the currency, rearranging French representation within the Central Bank of WAEMU, and modifying the control of the French Treasury over the foreign reserves of these states.

These propositions completely ignore the key aspects of the financial and monetary arrangements that many economists criticize: the existence of a formal link of monetary subordination between France and the CFA countries, the fixed parity with the euro, the freedom of transfers, and the existence of two monetary unions that have no other foundation than colonial history.

While the abandonment of the CFA franc does not guarantee that its member countries will develop rapidly with inclusive economic growth, fair distribution of income, and alleviating poverty, the extension of its life expectancy can hinder any prospect of political and economic sovereignty of these countries.

III/ Reform of the CFA Zone

Against this background and considering the cost and benefit analysis performed for the WAEMU economies in general and Senegal particularly, a debate about the dismantlement of the CFA zone is still ongoing among economists and policymakers. The debate is about whether to stick to the existing framework of the CFA franc and change some key features or leave the CFA franc zone. The abandonment of the CFA franc to choose an exchange rate regime will be based on lessons learned from the experience of the economic performance of floaters (countries that allow their currency to fluctuate) and peggers (countries that fix their currency against a major currency or a basket of currencies). Should Senegal advocate for a reform of the CFA (opt out for a break with the peg and envision a semi-flexible or flexible system) or get out of the Zone and adopt its national currency to regain its sovereignty over monetary policy and exchange rate policy? What is the best choice for Senegal?

Short Term: Overhauling the exchange rate framework.

As the CFA members countries in general and Senegal in particular, plan for a post-COVID-19 to grow their economies and alleviate poverty, meaningful reform of the CFA franc zone should be on their agenda instead of what the French president and the Ivorian president proposed in December 2019 ( revision of the monetary cooperation agreement with France as was the case in 1973 after the criticisms of president Eyadema and the renaming of the currency from CFA franc to Eco to take into account the political and identity dimension of money; the end of the centralization of BCEAO’s foreign reserves with the French treasury (hence the closing of the operation account); and the withdrawal of France from the board of directors, the BCEAO monetary policy committee, and the WAEMU banking commission. This proposed reform is not enough and is meaningless. Consequently, one can envision a reform of the Zone since the inflexible CFA Franc monetary and exchange rate arrangement is a major contributor to the lagging economic performances (lower real GDP growth, lower per capita real GDP, lower HDI, higher trade deficit, less FDI) of countries such as Senegal, besides other factors such as bad governance, systemic corruption, inadequate business regulatory environment, human capital building, and a lack of investment in infrastructure.

The current exchange rate framework should be changed to reflect greater monetary flexibility, the possibility of improving competitiveness, adopting export-led growth, and realigning incentives for agricultural producers. To reach these goals, the exchange rate regime should evolve from the peg to the euro because anchoring the CFA to the euro no longer has the same meaning nor does it serve the same interest as it did when the system was set up – export to eurozone has decreased by more than 50% and is currently at about less than 20%. This rebalancing of the trade pattern in favor of China, India, Thailand, and Nigeria justifies a new anchoring of the CFA to a basket of currencies, especially the euro, dollar, and renminbi, reflecting WAEMU’s changing trade patterns with the rest of the world. The price of crude oil can be included in the basket to figure out the value of the exchange rate within a predefined band. Therefore, the benefits in terms of exchange rate stability with the euro are less effective due to less trade between the two zones.

Furthermore, there is a probability of a decrease in value in terms of export earnings because earnings are reported in USD, which must be converted to euros. So, an appreciation of the euro will lead to a decrease in the value of export earnings. It is also detrimental to the level of competitiveness because of the appreciation of the real exchange rate[4], and the only way to offset this negative impact on the level of competitiveness is to improve the term of trade by increasing the price of commodity goods which these countries do not control. This situation has led to a structural current account deficit since the introduction of the euro. It should also be noted that the peg to the euro creates a sentiment of “abandonment of monetary sovereignty” because of the need to follow policies set by the ECB to keep parity. Hence the restrictive policies of the Central Bank of WAEMU that explain the underfinance in these countries are the result of the peg. Indeed, M2/GDP is only 16%, which indicates a very low level of financing of economic activities.

Another reason for moving away from the peg is related to the concept of “optimal” currency area- the geographical region of the CFA zone is far from optimal due to three factors: (i) weak intraregional trade within WAEMU (it is less than 12% of total trade and well below the aim of 25%), (ii) less financial integration between the economies of WAEMU, and (iii) diverse capabilities to deal with asymmetric shocks (supply shocks such as oil shocks, COVID pandemic, or Ukraine war).

Moreover, suppose one uses exchange rate misalignment to measure the level of competitiveness of the CFA zone countries. In that case, there is a significant difference between countries in the zone, making it impossible to set up a single consensus monetary policy.

Finally, the goal of balancing stability and flexibility should make the currency more market-based to support exporters and entrepreneurs with the exchange rate adjustment. On the other hand, regaining monetary sovereignty can widen the options for fiscal and monetary management in a post-pandemic world.

Long Term: Adopting a national currency and setting up the required conditions for an independent central bank of Senegal.

As proved above, the CFA franc’s current financial and monetary arrangement is not conducive to economic growth and development because it hampers exports, hinders investment and industrialization, and creates inflationary pressure due to high inputs prices and commodities prices as well. More than sixty years after political independence or sovereignty, countries like Senegal no longer need neocolonial guarantees for monetary and fiscal management in conducting monetary and exchange rate policies. Overall, compared with the other African countries, economic growth and poverty alleviation, the human development index in the CFA franc zone has been lower since the 1990s due to the prohibitive cost of doing business in a currency pegged to the euro and because of restrictive monetary policies (tight credit policies) in the zone.

This monetary arrangement prevents the possibility of using big-push investments to transform the economies of the CFA countries, because of the fear that has been created in the minds of political leaders, policymakers, and economic managers of the zone by emphasizing the disadvantages of getting out of the Franc zone. But the lessons from the Asian tigers and many Latin American countries and African countries that manage their currencies should convince Senegal that it is possible to overcome the difficulties of having your currency and to manage monetary policy correctly to reach the stated economic goals of economic growth, price stability, job creation, and poverty alleviation.

Our advice to the future Senegalese government is to start overcoming the burden of this financial and monetary arrangement and start a timeline of setting up the prerequisites (such as setting up an independent central bank modeled after the Federal Reserve system and the institutions to manage our currency). It is time to regain our economic and monetary sovereignty. Senegal has the human resources needed for successfully managing a national currency.

References

1. Public Announcement of Macron/ Ouattara July 2019

2. Souleymane Gueye. “La devaluation du franc cfa: Mesure inevitable ou imputable à l’intersyndicale” published in Walf Quotidien 1993

3. The new terms of the arrangements between the countries in the CFA franc zone and France remain opaque and largely undisclosed. While the latest annual report states that the operating account that previously sat at the French treasury has now been closed since April 2021, it does not disclose the details of the new ways through which the CFA is still guaranteed by the Euro now that the reserves are no longer held at the French treasury.

4. Paul R. Mason and Catherine Pattillo. The Monetary Geography of Africa Brookings Institution Press

5. The view tends to be mercantilist and monopolistic in favor of French state-backed private multinationals that operate within the WAEMU area.

6. Many African countries – Sierra Leone (44.8%), Ghana (43.1%) Gambia (17.8%), and Nigeria (24.08%) – have experienced prolonged periods of inflation. These rates are well above the inflation rate in the CFA zone in general and Senegal (14.1%) in particular. This rate is expected to slow down to 9% in 2023. These high inflation rates result from supply chain disruptions, global commodity price fluctuations, rising food and energy prices, political instability, and currency devaluation in countries with flexible exchange rates.

7. Souleymane Gueye. Senegal: Corruption, Bad Governance, and Development Outcomes. L’Afrique des idees. 2023.

8. World Bank Development Indicators and IMF: Debt, trade deficit, and other economic indicators

9. Souleymane Gueye. The Determinants of Capital Flight in the West African Economic and Monetary Union. Updated working paper. Berkeley 2021.

10. “Africa’s last colonial currency: The CFA franc story” by N’dongo Sylla et Fanny Pigeaux

[1] See for example ‘Francs CFA: Les termes nouveaux d’une question ancienne’ de Kako Nupukpo, Demba Moussa Dembele and Martial Ze Belinga, or the book “Africa’s Last Colonial Currency: the CFA Franc Story’ by Fanny Pigeaux and Ndongo Samba Sylla, among recent publications on the topic.

[2] Special Drawing Rights are assets created by the International Monetary Fund (IMF) and act as potential claims used by WAEMU countries to supplement their official reserves.

[3] The two sub-zones are the WAEMU (West African Economic and Monetary Union) and CAEMC (Central African Economic and Monetary Union).

[4] This real exchange rate is the Nominal exchange rate*(domestic price/ foreign price).

Laisser uncommentaire

Votre adresse e-mail ne sera pas publiée. Les champs obligatoires sont indiqués par *